After the pandemic, savings rose, with savings rate trends diverging slightly from their respective peaks between the United States, Europe, and the United Kingdom.

to Savings rates was the basis for sustaining growth Post-Covid-19. This is especially important in developed economies, where consumption averages 70% of GDP. As governments around the world provided support in different ways during the pandemic, savings rates doubled in some countries. It was a historical event.

This is because incomes have been supported by government transfers while spending has fallen due to both uncertainty and restrictions. However, it is worth noting Savings trends differ slightly between the US, Europe and the UK. There have been changes. And they are relevant.

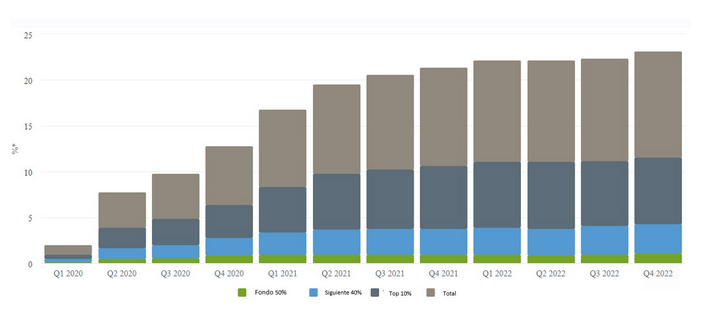

Savings as a percentage of disposable income

“US consumers fell below their pre-pandemic spending and savings guidelines, while German, French and British consumers did not. As consumption represents a large portion of GDP in these economies, the impact on growth is more significant. This is one of the factors that explains why US growth has been stronger than that of Europe in recent quarters,” explains Felipe Villaroyal, portfolio manager at Twentyfour AM (Vontobel).

The European case

The European case deserves deeper study. Between 2015 and 2019 the savings rate in the European region averaged 12.6% of disposable income. This changed with the onset of the pandemic, rising to 25.4% in the second quarter of 2021.

During pandemic lockdowns, people were able to buy durable goods, but in most countries were unable to go to restaurants, go on vacation or go to the hairdresser. While economic output has slowed due to Covid, most revenues have remained the same. Also, there has been no significant increase in unemployment rates in the eurozone as governments have come to the rescue with generous job-severance programs.

Savings increased manifold due to lower expenditure and solid income. According to ECB calculations, the excess savings rate increased to 11.3% of total disposable income between the first quarter of 2020 and the fourth quarter of 2022. “It is very important at the start of the economic recovery to strengthen private consumption,” says Ulrike Gastens. This was a major factor.

As the DWS economist explains, The scene has changed since then. Households invested their savings in housing and financial assets such as stocks and bonds and used them to repay loans. Meanwhile, liquid assets such as cash or bank deposits, which are readily available for consumption, have shrunk steadily, from a peak of 3.7% of disposable income in the first quarter of 2021 to just 0.6% in the fourth quarter of 2022. “This means there are no savings or assets that can be easily converted into spending money.” In the states.

A different pattern in rich families

A Savings distribution Availability is also important. “Calculations by the Monetary Authority show that wealthier households continue to keep savings in the bank. While the richest 10% of the population accounted for less than half of savings in the first quarter of 2020, this figure has risen to almost two-thirds in the fourth quarter of 2022.

However, wealthier households have a lower marginal propensity to consume and react more slowly to changes in their wealth. The opposite is generally true for less affluent and lower income groups. “When they have money, they spend it.”

“All this means that available savings are no longer an additional source of stimulus for consumer spending and growth. But with inflation expected to ease significantly in the coming months, at least real income growth could pick up again, which should help consumers and the overall economy a bit. But the unexpected Covid bonanza has come to an end,” he concludes.

Distribution of accumulated savings by family groups

“Internet evangelist. Writer. Hardcore alcoholaholic. Tv lover. Extreme reader. Coffee junkie. Falls down a lot.”

More Stories

Manta Ray | An autonomous Stingray-shaped drone has completed testing in the US

Historical flaw: Brazil loses the territory of Brera to the United Kingdom in a territorial dispute that highlights the effects of British imperialism on demarcating borders in South America

USA: Number of arrests in pro-Palestinian protests at universities exceeds 2,300.